Navigating the world of car insurance can be confusing, especially with Michigan’s unique regulations. Whether you’re a new car owner, a student, or simply looking to make sure you’re getting the best deal, understanding your options is crucial.

In Michigan, every driver is required by law to have car insurance. The state uses a “no-fault” system, meaning that your own insurance covers your medical expenses and other losses after an accident, regardless of who caused it. This approach is designed to reduce legal battles and speed up claims, but it also means higher insurance costs.

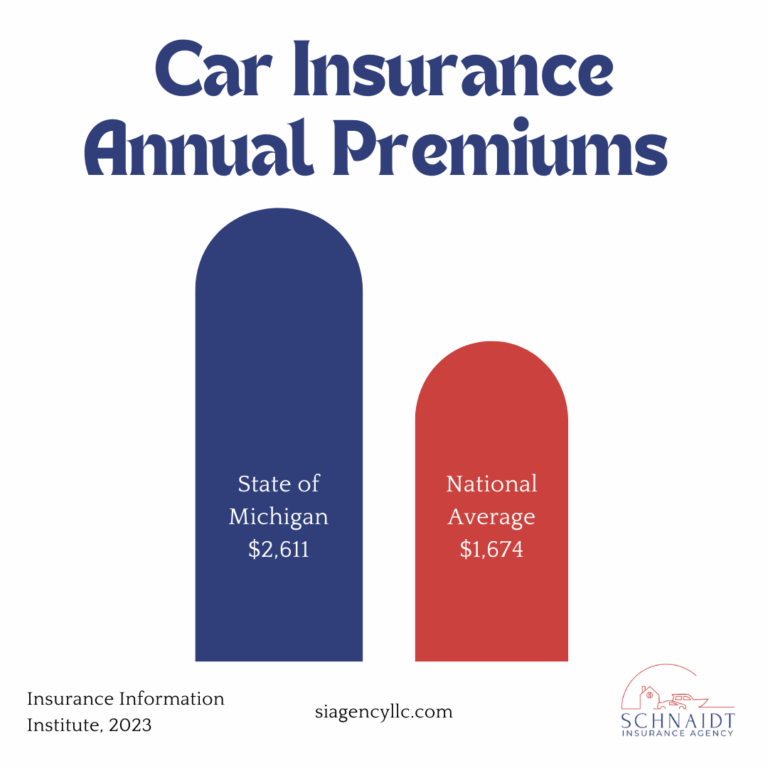

In fact, Michigan often ranks among the states with the highest car insurance rates, with an average annual premium of around $2,611 in 2023, compared to the national average of $1,674. This makes understanding your options and choosing the right coverage even more important【source: Insurance Information Institute】.

This coverage ensures that, in the event of an accident, your own insurance pays for your medical expenses and lost wages. This policy reduces the need for lengthy lawsuits, but it also means that Michigan drivers often need to carry more coverage than in other states.

PIP covers your medical expenses, rehabilitation, and even some non-medical costs like lost income. The level of PIP coverage you choose can significantly impact your premium. Recent changes to Michigan’s no-fault law allow drivers to select different levels of PIP coverage, potentially lowering costs.

This covers damage your car causes to other people’s property (like buildings or fences) up to $1 million. It’s a unique feature of Michigan’s insurance laws, separate from liability insurance that typically covers such damages in other states.

Although Michigan’s no-fault law limits lawsuits, you can still be sued for damages in certain situations, such as when someone is seriously injured. BI/PD covers these legal liabilities and associated costs.

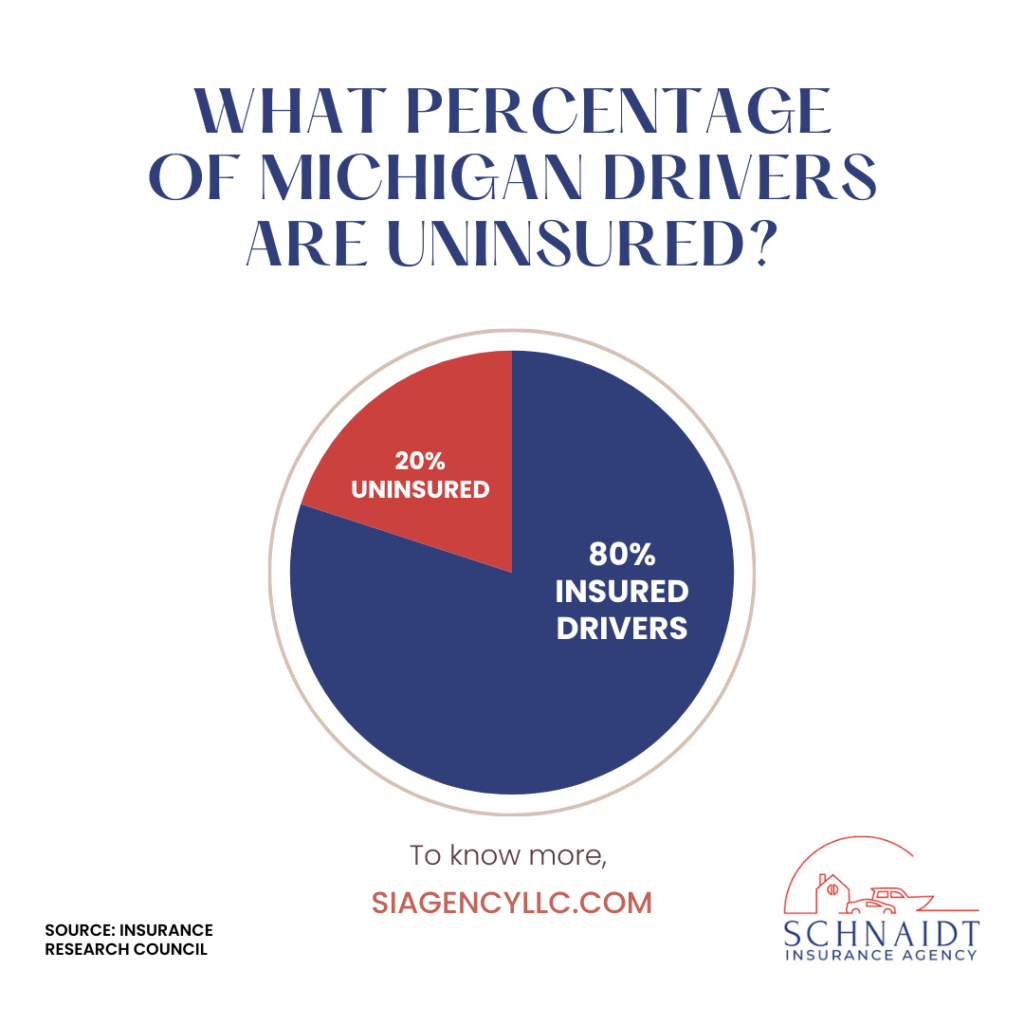

With around 20% of Michigan drivers estimated to be uninsured, this coverage protects you if you’re hit by a driver who doesn’t have adequate insurance【source: Insurance Research Council】.

This optional coverage pays for damage to your vehicle caused by non-collision events—like theft, fire, or hitting a deer (common in Michigan). Given Michigan’s variable weather and high deer population, comprehensive coverage can provide essential peace of mind.

Covers repairs to your car if it’s damaged in an accident, regardless of fault. It’s particularly useful for newer cars or those financed through a loan or lease.

Combines comprehensive and collision insurance with Michigan’s mandatory coverages. While “full coverage” isn’t an official term, it’s a good way to describe a policy that offers broad protection.

This optional add-on helps cover medical expenses after an accident, regardless of fault. It’s different from PIP and might have lower limits.

If you’re financing or leasing a car, gap insurance covers the difference between what you owe on the vehicle and its current market value if it’s totaled. This is especially valuable for newer cars, which can depreciate quickly.

Understanding your coverage options can help you make the best choice for your situation:

Meets Michigan’s minimum requirements (PIP, PPI, BI/PD). This is the most affordable option but may not provide enough coverage for major accidents.

Includes the basics plus uninsured/underinsured motorist coverage. It offers a balance between cost and protection, especially if you’re worried about encountering uninsured drivers.

Adds comprehensive and collision coverage to the basic plan. This is ideal for newer cars or drivers who want to protect their vehicle from a wider range of risks.

Often includes all of the above plus extras like rental car reimbursement or towing. This is suitable for those who want maximum peace of mind.

Many insurers allow you to tailor your policy to suit your needs, whether that means lowering your deductible or bundling multiple types of insurance for a discount.

You’re unique and so is your car. Just like this unique AI generated image. If you think a custom auto insurance plan might be right for your uniqueness, Schnaidt Insurance Agency does offer custom plans.

Insurance premiums in Michigan are influenced by several factors:

A clean driving record typically results in lower premiums, while accidents or violations can lead to higher rates.

Insurers often use credit scores as a factor in setting rates. A higher score can mean lower premiums.

Urban drivers might pay more due to higher rates of accidents and theft.

Cars that are more expensive to repair or have higher theft rates often come with higher insurance costs.

Younger drivers, particularly males, generally face higher rates due to perceived risk.

Consider factors like your vehicle’s value, your driving habits, and your financial situation.

Use comparison tools and get quotes from multiple insurers to find the best rates.

Many insurers offer discounts for things like bundling policies, being a good student, or having safety features in your car.

Your insurance needs can change, so it’s wise to review your policy each year to ensure it still meets your needs.

In 2020, Michigan passed significant reforms to its auto insurance laws to reduce costs. These changes give drivers the option to choose lower levels of PIP coverage, which can lead to lower premiums. However, selecting a lower PIP level means less coverage for medical expenses, so it’s important to weigh the potential savings against the risk of higher out-of-pocket costs in the event of a serious accident.

Choosing the right auto insurance can be overwhelming, but working with an experienced insurance agent can make the process easier. A good agent can help you understand your options, find discounts, and select the best coverage for your needs.

At Schnaidt Insurance, we’re here to help you navigate Michigan’s auto insurance landscape. Our team is dedicated to providing personalized service to ensure you have the coverage you need at a price you can afford. Learn more about our team here.

Auto insurance isn’t just a legal requirement in Michigan; it’s a critical part of protecting your financial future. By understanding the various types of coverage and how they apply to your situation, you can make informed decisions that provide peace of mind on the road.